Capital

Or, How the Smart Money Got China Spectacularly Wrong While Calling India a Bad Bet

This is the umpteenth in a series exploring India’s contradictions. In previous posts we looked at why India’s soft power travels and China’s doesn’t. This post is the sequel: the same civilizational defaults — India outward, China inward — that explain why a Russian figure skater wore a bindi at the Olympics also explain something larger and more expensive. They explain why, for thirty years, the smartest capital on earth ran in the wrong direction.

I. The Building Floor

My former business partner invested in China.

His Chinese partner took the money. He protested. His Chinese partner pointed out the window.

“See that building? I built it with your money. The top floor can be yours.”

My partner, gently, said that wasn’t really why he had wired the funds. The Chinese entrepreneur was unmoved.

“Yes, and so?”

So my partner did what any grown adult in possession of a contract and a few good lawyers would do: he sued. In a Chinese court. And here is the part I want you to sit with for a moment: the court agreed that all the facts were in his favor. Every one of them. The court congratulated him on the quality of his case. And then the court left the money with the Chinese entrepreneur anyway, on the theory that the Chinese government did not want the capital flowing out of the country.

So: the facts were yours. The verdict was, in some sense, yours. The money was not yours.

You got a floor. In a building. In a city you didn’t live in.

My partner has since passed away. He died knowing he had been cheated. He died knowing the legal system had agreed he had been cheated. He died knowing that none of that mattered, that nothing was ever going to come of it, and that there was no further recourse, in this life, against the people who had taken his money. That is a very bitter pill to swallow at the end. It is the kind of bitter pill that I want any reader of this post to take seriously, before we get to the part where we laugh at hedge fund managers. Because everything that follows in this post — the data, the comedy, the booster-class roast, the civilizational thesis — sits on top of a small number of specific individual human beings who lost specific individual sums of money and never got them back, and who, in some cases, died waiting.

I have heard a lot of stories in my life, but this one has stayed with me, because it perfectly compresses something that took American capital roughly thirty years and several trillion dollars to discover: in China, the courts can rule for you and still rule against you. You will be told you are correct. You will be congratulated on the elegance of your arguments. And then you will be invited to look at the lovely building. And then, if you are unlucky, you will die before anything else happens.

For most of my adult life, the smart money on Wall Street believed the smart play was China. India was viewed as the slow uncle at the wedding — well-meaning, voluble, eventually charming, but somebody you certainly weren’t going to entrust with serious cash. China was the cool young cousin with the MBA and the gym membership. China was the future.

I have, for thirty years, told anyone who would listen one simple piece of investment advice: invest anywhere you want, but not in China. I was, for most of those thirty years, considered a crank. Slightly cracked. Probably resentful of Chinese success for ethnic-Indian reasons that I had not fully examined.

So let us now examine the people who were not considered cranks. Let us examine the smart money.

II. The Numbers Behind the Mistake

The data, before the comedy.

At the end of 2023, the US Bureau of Economic Analysis reported that the American direct-investment position in China stood at $126.9 billion. The corresponding figure for India: $49.6 billion. A ratio of 2.6 to 1. American capital had committed roughly two and a half times as much to the country actively designed to keep capital from leaving as it had to the country whose laws permitted capital to come and go through the front door.

This made no sense even on the simplest metric, return on capital. US-owned affiliates in India earned $7.9 billion in 2023, against $11.3 billion in China — meaning India produced about seventy percent of China’s income on thirty-nine percent of the invested stock. In 2023, and on the available evidence for a good while before it, India was simply the better trade per dollar deployed. Not by a little. By a lot.

Then, in 2023, the arrow finally turned. In the BEA data, new US direct-investment financial flows into India ($6.0 billion) exceeded new flows into China ($5.1 billion) for the first time. Separately, on China's own balance-of-payments measure, inward direct investment went negative in the third quarter of 2023 — minus $11.8 billion — the first negative quarterly reading in roughly twenty-five years of that series. Different official datasets measure FDI differently, and they do not always agree on the magnitude; China's Ministry of Commerce reports a higher "utilized FDI" number than the balance-of-payments series does. But the direction of travel is no longer ambiguous on any of them. The China premium is becoming an exit discount. India, meanwhile, crossed a cumulative trillion dollars in inward FDI in October 2024, and reported roughly $81 billion in inflows for the 2024-25 fiscal year.

Capital is supposed to be efficient. Capital is supposed to know things. Capital is supposed to vote with its feet. So what does it mean when the smartest capital on earth spent twenty-five years voting with its feet into a country whose system, on inspection, was specifically designed to prevent capital from ever voting with its feet again?

It means, technically speaking, that the smart money was full of shit.

Let us examine some of the relevant shit.

III. The Booster Class

The roll call of public China bulls over the past two decades reads, in retrospect, like a tour through the wing of an asylum reserved for people who got everything wrong but were paid extremely well to be wrong in expensive suits.

Jim Rogers. Co-founder of the Quantum Fund with George Soros. One of the most celebrated investors of his generation. In 2007, he moved his family from New York to Singapore specifically so his daughters would grow up speaking Mandarin — the air pollution in Beijing and Shanghai having put those cities out of contention as the actual destination. In the same year, he published A Bull in China: Investing Profitably in the World’s Greatest Market. I am not making the title up. There is also a sequel of sorts called Street Smarts, in which the bullishness continues unabated.

On India, Rogers was less effusive. In 2001:

“India as we know it will not survive another 30 or 40 years.”

In 2015, exiting the Indian market, he offered this elegant farewell:

“One cannot invest based on hope.”

On a CNBC interview in 2008, Rogers explained that he had moved to Singapore over Shanghai only because of pollution. Not because of the one-party state. Not because of the capital controls. Not because of the legal system that, as we shall see, regards foreign investors as a kind of voluntary tribute. The dictatorship was fine. The smog was unacceptable.

To his credit, by April 2024 Rogers had finally pivoted. He is now bullish on India. He cites Modi. He cites the convertibility issue. He is at long last on board with what some of us have been arguing since 1991. Welcome aboard, Jim. The party started thirty-three years ago. We saved you a chair.

Mark Mobius. Calls himself “the Indiana Jones of Emerging Market investing,” which is the kind of self-description that should disqualify a person from managing their own checking account, let alone other people’s. Ran Franklin Templeton’s emerging-markets desk for thirty years. Was, in his own publicity material, known for his bullish views on China.

Then, in March 2023, on Fox Business, Mobius reported the following discovery:

“I have an account with HSBC in Shanghai. I can’t take my money out. The government is restricting flow of money out of the country.”

This sentence is so good I want to needlepoint it onto a throw pillow. Notice the genuine surprise. I can’t take my money out. Mark Mobius has just been informed, in his late eighties, after a forty-year career as a celebrated emerging-markets specialist, that the People’s Republic of China — a one-party communist state that has imposed capital controls since approximately the Truman administration — is restricting the flow of money out of the country.

He went on:

“I can’t get an explanation of why they’re doing this... They’re putting all kinds of barriers. They don’t say: ‘No, you can’t get your money out.’ But they say: ‘Give us all the records from twenty years of how you made this money.’ This is crazy.”

This is crazy. Yes, Mark. This is crazy. This has been crazy for thirty years. The thing you wrote books about and earned management fees on for three decades was exactly this kind of crazy the entire time.

And then, having discovered — like Columbus, except with substantially less excuse — that the country was not arranged the way he had been telling everyone it was arranged, Mobius announced his new favorite emerging market:

“India... You’ve got a billion people, they can do the same thing that the Chinese do.”

Welcome aboard, Mark. We saved you Jim’s chair.

Mark Mobius died last month, on the fifteenth of April, in Singapore, at eighty-nine. He went out, by all accounts, bullish on India. The chair we saved him, in retrospect, was saved a bit late.

Stephen Schwarzman. Co-founder of Blackstone, currently $1.3 trillion in assets under management. In 2007, the Chinese sovereign wealth fund, China Investment Corporation, bought a non-voting minority stake in Blackstone's IPO — roughly 9.3 percent, carefully kept under the ten percent threshold that would have triggered a US national-security review. In 2013, Schwarzman announced a $100 million personal gift, plus a $200 million fundraising campaign, to build Schwarzman College at Tsinghua University in Beijing — a sort of Rhodes Scholarship for the China century. Its premise, in Schwarzman's own words:

“In the twenty-first century, China is no longer an elective course, it’s core curriculum.”

The advisory board includes Henry Kissinger, Condoleezza Rice, Hank Paulson, Robert Rubin, Colin Powell, Richard Haass.

Pause on what Schwarzman College actually represents. The largest internationally-funded philanthropic project in the history of the People’s Republic of China — over five hundred and seventy-five million dollars raised, with that advisory board reading like a roll-call of the postwar US foreign policy establishment — was created by an American private-equity billionaire to teach the next generation of Western elites that China was core curriculum. The college sits inside Tsinghua University. Tsinghua University is the campus where Xi Jinping went to school. The Schwarzman College buildings, designed by Robert A.M. Stern, sit on land that the Chinese state allowed to be allocated to a Western donor for the explicit purpose of credentialing future Western leaders inside a Chinese intellectual environment. The premise of the project was that the smart Western response to the rise of China was to deepen our understanding of it.

And while this enormous institutional bet was being placed in Beijing — over a decade, by some of the most credentialed figures in American public life, with the full and enthusiastic blessing of the Chinese state — the actual money was quietly moving in the opposite direction. Blackstone’s own internal reports were saying India. Not as a hedge. Not as a diversification play. As the best-performing market in the world.

“India has given us the strongest results across the world. And [I] am optimistic this [will] continue going forward.” — Stephen Schwarzman, Mumbai, March 2020.

In March 2025, Blackstone announced it intends to double its India exposure from $50 billion to $100 billion. By that point Schwarzman was personally announcing, in Mumbai, that he intended to put twice as much capital into India as Blackstone had ever put into China. The man who built the Rhodes Scholarship for the China century turned out, on inspection, to be a quiet bull on India. Possibly the largest one in the room. The hands and the mouth, working independently, possibly to the surprise of both.

And then there is Ray Dalio.

IV. Interlude — Ray Dalio Explains His Own Ideas

A short field trip.

Ray Dalio is the founder of Bridgewater Associates, the world’s largest hedge fund. He has written six books on Principles. He has, on multiple occasions, explained that he loves China — not metaphorically, but as a stated, formal reason for his investing decisions. In an April 2024 LinkedIn essay titled “To Answer the Question of Why I Invest in China,” the first reason Dalio listed was, in summary, love for China. Reason number two was that the country and its people were great. This is the man Wall Street took seriously on China for two and a half decades.

In December 2021, Dalio sat down with the economist Tyler Cowen — one of the most generous and well-prepared interviewers alive, a man who has a documented soft spot for India and who, when he asks you a question, has read every book on the table, including yours. What followed is, on the public record, instructive.

Exhibit A. Cowen asks the simplest possible question. The finance literature shows excess returns are very hard to predict. Dalio’s entire worldview is built on the idea that big macro forces — debt cycles, polarization, the rise of China — do predict where markets are going. So: do they? If yes, why doesn’t the research literature show that?

Dalio: “There are so many people who write finance papers, and then there are people who make money in the markets. I can’t speak for those who are writing the finance papers.”

Cowen presses. Dalio talks about debt cycles. Cowen presses again — if it’s publicly available information, why isn’t it already in prices?

Dalio’s final answer, in its entirety:

“Some can and some can’t. I guess you look at the track records over long periods of time, and you decide who can and who can’t.”

That is the response. The founder of the world’s largest hedge fund, asked to articulate his epistemic edge over the market, says: you look at the track records. The man who has written six books on Principles cannot, when politely asked, articulate a single Principle.

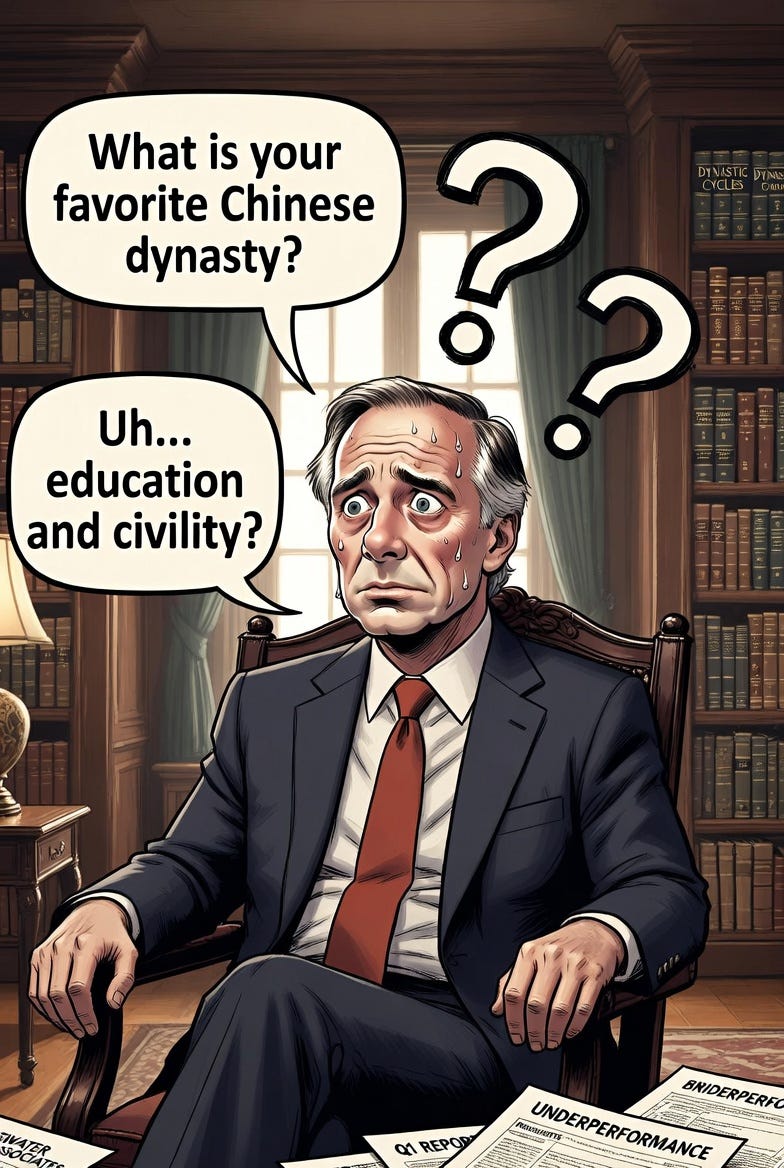

Exhibit B. Cowen, gently, hands Dalio what should be a softball:

“What is your favorite Chinese dynasty and why?”

Dalio has written a 500-page book that leans heavily on Chinese dynastic cycles. He has love for China. Surely he has a favorite.

Dalio’s answer runs over six hundred words. Across those six hundred words, he names zero favorite dynasties. He explains that he doesn’t really have a favorite. He gestures vaguely at “the Tang Dynasty, the Song Dynasty, the Ming Dynasty” without picking one or saying what he admires about any of them specifically. The closest he comes to substance is the observation that healthy dynasties had “education and civility” — a banality so spectacular it could be inscribed over the entrance of a community college lobby and would be considered, by the trustees, possibly too generic.

This is the man whose entire China thesis rests on a deep understanding of Chinese civilizational cycles. Asked to name his favorite Chinese dynasty, he cannot.

While Ray Dalio was being the smart money, Bridgewater’s flagship Pure Alpha fund underperformed the S&P 500 from July 2012 to August 2021 — nine consecutive years. In 2019, the leveraged version of Pure Alpha lost half a percent in a year that the S&P 500 returned 31.5 percent including dividends. Ray Dalio talks like the sage of the changing world order. Ray Dalio invests like a slightly underperforming index fund with substantially higher fees.

That is the level of intellectual seriousness Wall Street brought to the question of whether to send your retirement savings to Beijing.

V. What They Walked Into

Now, the system itself. Because this is where I want to be Milton Friedman for a minute, before going back to being Dave Barry. The Chinese system, on inspection, is not subtle. It was never subtle. The capture mechanisms have been hiding in plain sight for the duration. They are written in the law.

For most of the period from 1994 to 2022, a foreign automaker that wanted to build cars in China was required to do so through a joint venture in which the Chinese partner held at least half. GM-SAIC. Volkswagen-FAW. BMW-Brilliance. Toyota-FAW. Honda-Guangzhou. The ownership caps were lifted in stages — electric-vehicle makers freed in 2018, commercial vehicles in 2020, passenger cars in 2022 — but for the quarter-century that mattered, the rule held. The Western automakers brought the engineering, the manufacturing expertise, the brand, the supply chain knowledge, and the capital. The Chinese partners watched, took notes, and were given a quarter-century in which to absorb every transferable thing they could absorb. The five state-owned champions that emerged — SAIC, FAW, Dongfeng, BAIC, and Chang’an — now dominate the Chinese auto market alongside an indigenous ecosystem of competitors like BYD, Geely, Nio, and Xpeng that grew up in the shadow of these joint ventures, often staffed by engineers trained inside them. Today, in 2026, several of the original Western JV partners are being squeezed out of the Chinese market entirely, by Chinese champions raised on Western milk.

The same broad pattern appeared in aerospace. COMAC’s C919 is a Chinese aircraft, and the Chinese state is rightly proud of it — but its supplier stack leaned heavily on Western and Western-joint-venture components: engines from a GE-Safran venture, avionics from Honeywell, systems from Collins Aerospace. Boeing’s own joint venture with COMAC was a separate 737 completion-and-delivery center, not the C919. The point is not that Boeing secretly built China’s airliner. The point is subtler and more familiar: China built its competitor aircraft inside an ecosystem that Western firms had spent decades helping to assemble, and the Western firms handed over the components one purchase order at a time. Former US Deputy National Security Adviser Matt Pottinger told CBS News the C919 “looks like a knockoff.” It looks like a knockoff because a great deal of what is inside it came, by invitation, from the West.

Then there is the case of American Superconductor Corporation, which deserves a paragraph all to itself.

AMSC was a Massachusetts company that designed wind-turbine control software. Its largest customer was Sinovel, China’s biggest wind-turbine maker. In 2011, an AMSC engineer based in Austria, having been bribed by Sinovel, handed over the source code. When the theft surfaced, AMSC’s stock collapsed; the company lost the great majority of its market value over the following months, and laid off seven hundred people — more than half its global workforce.

In January 2018, a federal jury in Wisconsin convicted Sinovel of trade-secret theft. The court found AMSC’s losses exceeded $550 million. The maximum statutory fine the court was empowered to impose was $1.5 million. AMSC eventually settled for $57.5 million in restitution — roughly a tenth of what it had lost in a single trading session, and itself a recovery rate, on the court’s own damages finding, of about ten percent.

According to reporting from the time, Sinovel’s CEO Han responded to the early investigation by allegedly describing software as “like cabbage.” In China, software is like cabbage. You don’t pay for cabbage. You just take some.

This is the country into which Wall Street poured, by some estimates, eight hundred billion dollars in new investment between 2017 and 2020 alone.

And then there is the actual machinery of getting your money out. The People’s Republic operates a closed capital account, which is a technical term meaning that the State Administration of Foreign Exchange — SAFE, in a piece of regulatory nomenclature so on the nose it could have been written by a Jon Stewart writers’ room — must approve every outward flow of capital, dollar by dollar, audit by audit, year by year. Foreign companies wishing to repatriate profits must first pay twenty-five percent corporate income tax, then submit to a mandatory annual audit, then permanently allocate ten percent of their after-tax profits to a “Surplus Reserve Fund” — locked away in renminbi, in China, until that fund reaches half the company’s registered capital — and finally secure SAFE approval, which can take months. Dividends may only be remitted once per fiscal year.

If you try to route around this with intercompany service fees or royalties, you trigger an anti-avoidance audit. Anti-avoidance audits take years to resolve. While they are being resolved, you may not be permitted to leave the country.

Which brings us to exit bans. A 2024 Stanford Journal of International Law paper documented 128 foreigners — twenty-nine Americans, forty-four Canadians, the rest from elsewhere — placed under exit bans in commercial disputes between 1995 and 2019. The number is now believed to be much higher. The civil-society group Safeguard Defenders reports that exit-ban mentions in China’s official court database rose from fewer than five thousand in 2016 to thirty-nine thousand in 2020, and have doubled annually since.

A partial list of recent named cases, all of them foreign business executives:

Chenyue Mao, a managing director at Wells Fargo, banned from leaving China in July 2025. Allowed to return only in September 2025, after high-level US-China negotiations.

An Orange County businessman, the so-called “Horowitz” case from 2011, banned from leaving China after rejecting a defective Chinese supplier’s product. Released only after his wife wired $250,000 to the supplier whose product he had refused.

Richard O’Halloran, an Irish executive, held in China for three years between 2019 and 2022 over a Chinese partner’s fraud that he had not personally committed and could not have prevented.

There are many more. Bankers from Nomura. A US Patent and Trademark Office employee, on personal travel with his family. The five Chinese staff of the American due-diligence firm Mintz Group, detained for two years between March 2023 and March 2025. The firm itself was fined $1.5 million for “unauthorized statistical investigations” — an offense which, by the standards of jurisprudence, has the same precise definition as “vibes the state did not like.”

A commercial-law professor at Columbia, writing on the school’s Blue Sky Blog in 2024, summarized the operational reality this way: an exit ban can be enforced against an individual executive of a US company when an ordinary commercial dispute arises. The Chinese company involved can ask a court to impose the exit ban through a formal legal process that occurs unbeknownst to the party whose exit is to be barred.

You only discover you cannot leave when you try to leave. Or, as the Eagles put it in a song that, on reflection, may have been about the People’s Republic of China all along: you can check out any time you like, but you can never leave.

And then there was Evergrande. The Chinese property developer, formerly the country’s largest and a perennial fixture in JPMorgan’s emerging-market bond indices, defaulted in 2021 with $300-plus billion in liabilities. Foreign bondholders held about $19 billion of the offshore exposure. The bonds traded at 2.25 cents on the dollar in late 2023. A Hong Kong court issued a winding-up order in January 2024. The order has “limited recognition” in mainland China — where ninety percent of Evergrande’s $242 billion in assets are physically located. Effective recovery for foreign creditors: approximately one cent on the dollar.

If you lent Evergrande a million dollars, you got back enough for a moderately priced lunch in midtown Manhattan.

This is what Wall Street, for a decade, called China’s investment-grade bond market. This is what Ray Dalio called China being tremendously successful in many different ways.

VI. The Country the Smart Money Missed

Now, for contrast, India.

India’s bureaucracy is real. India’s tax authorities are aggressive in a way that produces, on a recurring basis, international incidents and full-blown investor revolts. India self-inflicted, in 2012, a retrospective-tax amendment that effectively reached back five years to tax Vodafone’s already-completed acquisition of Hutchison’s Indian assets. The amendment also caught Cairn Energy, the British oil company. The international investor community lost its mind. Both companies took India to international arbitration. This is the kind of self-inflicted regulatory wound that, in many countries, would simply end the conversation about foreign investment for a generation.

And then something happened that has not happened in the People’s Republic of China in living memory.

Vodafone won at the Permanent Court of Arbitration in 2020. Cairn won $1.2 billion plus interest at the PCA in December 2020. India initially refused to pay. Cairn began enforcement actions, seizing Indian government-owned property in France. And then, in August 2021, India did what no closed-capital-account state ever does. The Government of India repealed the law. The Government of India paid. Cairn received roughly ₹7,900 crore — approximately a billion dollars — back in its bank account. Seventeen companies caught in the retrospective tax dragnet were absolved.

The system bent. The system paid. Because the system, however maddening on a day-to-day basis, is one in which international arbitration awards eventually have to be honored. India is a country in which, after the tax authority has tortured you for nine years, the courts may eventually rule for you. And when they do — and this is the part that should be carved into a wall somewhere on Wall Street — you actually get your money.

Compare this to Evergrande. Compare this to AMSC. Compare this, especially, to a man who died in his own bed in his own country knowing that a Chinese court had agreed he was right and that none of that had ever come to anything.

In India, you are slowly audited but can fight and get your money. In China, you are slowly eaten and will have nothing left to get.

The roster of foreign-corporate India operations that have run, without ever having a Mintz Group experience, is now extensive. Walmart bought seventy-seven percent of Flipkart for $16 billion in May 2018 — the largest e-commerce M&A in Indian history. The Competition Commission of India approved it, despite vocal opposition from domestic trader associations. Imagine, for a moment, the Chinese state regulator approving a $16 billion American acquisition of the leading Chinese e-commerce platform. Spend a minute with that mental image. Take your time.

Walmart has since spent another $3.5 billion to take its stake to roughly eighty percent. Amazon has invested approximately $11 billion in India to date, with $15 billion more committed by 2030. Google announced a $10 billion India Digitization Fund in 2020. Microsoft is in the middle of a multi-billion-dollar Azure expansion. Apple's revenue in India grew 36 percent year-over-year to roughly $8 billion in FY24, making India Apple's fastest-growing major market. Foxconn is scaling iPhone assembly in Tamil Nadu at a pace that has begun to alter Apple's global manufacturing geography.

None of these companies has had to wire $250,000 to a domestic supplier to recover a missing executive.

There is one more observation worth pausing on, because it is the consumer-side expression of the same civilizational difference.

Nike’s revenue in China is down twenty-eight percent from where it was five years ago, even as China’s overall sportswear market has boomed. Nike’s stock just hit a decade low. The company has laid off fourteen hundred people and jettisoned its longtime China leadership. Starbucks has sold a majority stake in its China operations to a local partner. Guess closed all of its more-than-one-hundred-fifty Chinese stores this past March. American automobile brands have been hammered by Chinese EV companies. Anta, formerly a domestic Chinese shoe brand, is now the largest shareholder in Amer Sports — which is to say, the Chinese athletic conglomerate owns Arc’teryx and Wilson. The high-end Western brands Americans buy at REI are, beneath the logos, Chinese. (The Nike data, and a great deal more, comes from a recent Wall Street Journal investigation — well worth reading in full.)

The proximate cause is a Chinese consumer-side phenomenon called guochao — a state-amplified wave of cultural-pride-driven preference for domestic over foreign brands, occasionally weaponized into formal boycotts when a Western company says something the state does not like about Xinjiang or Tibet or Taiwan. Foreign brands in China now operate in a market where loving the domestic brand is patriotic and buying the foreign brand is, depending on the political weather, mildly suspect.

In recorded Indian history, with one exception detailed below, no government — including the current Modi government, which is the most assertively Hindu-nationalist administration modern India has produced — has ever told Indian consumers that buying foreign brands is unpatriotic. Apple’s revenue in India is growing thirty-six percent a year. KFC operates extensively across the country. McDonald’s, Domino’s, Subway, Starbucks (yes, the same Starbucks that just sold its China business), Levi’s, Zara, H&M, Uniqlo, Nike, Adidas — all of them operate, profitably, in Indian cities. Mumbai is full of Mercedes-Benz dealerships. Delhi is full of BMW showrooms. India certainly has nationalist economics — swadeshi sentiment, “vocal for local” campaigns, periodic boycotts of Chinese goods in particular. What India has never produced is a durable, state-amplified consumer movement of the Chinese kind: the kind that can turn a global brand into a patriotic liability overnight and keep it that way. There is no durable Indian guochao, there has never been one, and there is unlikely ever to be one, because Indians want the best product available, do not particularly care where it comes from, and have been consistent on this for a very long time. The Indian state can do many things. It cannot turn off the Indian consumer’s millennia-old willingness to buy whatever is good, from whoever is selling it, at whatever price clears.

The one period in modern Indian history when Indians were not allowed to buy foreign brands was the era between roughly 1969 and 1991 — when the Indian state, briefly persuaded that Soviet-style autarky was the path to prosperity, expelled Coca-Cola and IBM in 1977, restricted imports through the Foreign Exchange Regulation Act, and tried to manufacture everything domestically behind a wall of tariffs and the License Raj. The result was a national catastrophe. Indians spent twenty-two years standing in line for badly made domestic substitutes they did not particularly want, while their cousins overseas drove imported cars and drank imported soft drinks. The 1991 reforms — which I have covered at length in Posts 19A through 19C — stuck, and have stuck for thirty-five years now, against the explicit ideological preferences of every successive Indian government including the present one. They stuck not primarily because economists won the argument but because the Indian population had personally experienced the consequence of being forbidden to buy foreign brands and had no interest in repeating the experience.

The political mechanism by which Coca-Cola was kicked out of India is worth a brief detour, because it illustrates the breadth of the failure across the Indian political class. The Foreign Exchange Regulation Act — the law that required foreign companies to dilute their Indian operations to forty percent local equity, and that demanded, in Coca-Cola’s case, that the secret formula itself be handed over to an Indian state-monitored body — was passed in 1973 by Indira Gandhi’s Congress government. Coca-Cola refused to comply and continued negotiating. Two years later, in 1975, Mrs. Gandhi declared a national Emergency and suspended Indian democracy outright. Two years after that, in 1977, the Indian electorate threw her out in favor of a coalition — the Janata Party — that had been specifically organized to reverse her authoritarian excesses. The new Prime Minister, Morarji Desai, and his Industry Minister, George Fernandes, then proceeded to take office and not undo FERA but, instead, to enforce it more strictly than Mrs. Gandhi had ever bothered to. Coca-Cola and IBM were given ultimatums. Both refused to comply. Both left.

The timeline, summarized, reads: the ruling party writes the rule, suspends the constitution, loses the next election to the people who had organized themselves around the explicit promise of fixing her, and the new government — having taken office on a wave of national revulsion against Mrs. Gandhi’s overreach — then keeps one of her economically dumbest rules and uses it to expel Coca-Cola. This is not one party’s blunder. This was the entire Indian political class, across every available faction, displaying a remarkable bipartisan inability to operate within their own civilization’s five-thousand-year-old operating system. The civilization had run the largest trading economy on earth. The civilization had been operationalizing Ricardo since the Mauryan period. None of that information appears to have penetrated to the Lok Sabha in either 1973 or 1977. Both parties, in succession, failed at being India.

Indians remember what closure tastes like. It tasted like Campa Cola. It could, alternatively, have tasted like the urine of the Prime Minister of India — Morarji Desai, who expelled Coca-Cola from the country in 1977 and who, in his spare time, drank his own urine daily for health and recommended the practice to Dan Rather on 60 Minutes in 1978. The official position of the Government of India in the late 1970s was, on the available evidence, that piss was healthier than sugar. Indians, alone in the world in this assessment, respectfully disagreed. They have been disagreeing, in increasing volume, ever since. They are not eager to find out what closure tastes like again.

That is, in significant part, why foreign capital makes money in India and is permitted to leave with it. The Indian consumer demand for foreign products is itself a civilizational artifact older than the Indian state. The state cannot suppress what it did not create — and the one time the state tried, the population eventually voted, in 1991, to never let the state try again.

The Chinese state, by contrast, can and does turn consumer behavior on and off like a faucet. Capital in China cannot leave because the state will not let it. Foreign consumer brands in China cannot earn because the state has decided they should not. The two phenomena are, civilizationally, the same phenomenon — and a five-thousand-year-old open trading society would never tolerate either.

VII. The Pattern Recognition Problem

Here is the thing I think actually explains the whole story.

The smart money on Wall Street has not been dealing with the Chinese for very long. A few decades, in earnest. Long enough to write some books with foolishly confident titles. Not long enough to recognize a pattern.

The Indians have been dealing with the Chinese for a very long time. The Indian merchant class has been trading along routes that touched Chinese trading partners since the early days of the Silk Road — at least the second century BCE, well before there was a country called the United States, before there was an England, and roughly contemporaneously with the Roman Republic. Indian traders along the Silk Road, Tamil merchants in Southeast Asia, Marwari and Gujarati traders moving silk and spices across the Indian Ocean, Parsi merchants in Hong Kong and Canton in the eighteenth and nineteenth centuries — there is no generation of Indian commercial life in living civilizational memory that has not, at some point, encountered the Chinese system.

Here are two facts that the modern China booster ought to know and, on the available evidence, does not. The English word Mandarin comes, through Portuguese mandarim and Malay menteri, from the Sanskrit mantrī — “counselor,” “minister of state” — and entered English in the 1580s. The English word China has a more contested path; most authorities trace it ultimately to the Qin dynasty, but the form that carried that name westward, into Persian and onward to Europe, was the Sanskrit Cīna. Both words are roughly five centuries old in English, and both reached English through the channels of Indian and Indian-Ocean commerce rather than through any direct European contact with China. The Westerner who today announces that he is bullish on China, and that he is having his children learn Mandarin, is — without knowing it — describing his enthusiasm in vocabulary that came west along Indian trade routes. India did not need Goldman Sachs to introduce it to China in 1997. India had been the West’s interpreter of China since before the East India Company was chartered. If you want to understand how China treats the outsider who arrives to do business, the people to ask are not the ones who showed up in the 1990s with a Bloomberg terminal. The people to ask are the ones who supplied the vocabulary.

And the Chinese system, on every one of those encounters, has done what the Chinese system does. It captures. It absorbs. It treats foreign commerce as a temporary accommodation to be terminated at the convenience of the state.

Consider the Canton System, which the Qing imposed from 1757 until the First Opium War in 1842. Western traders — British, Dutch, French, eventually Americans, and a substantial Parsi contingent from Bombay — were restricted to a single port, Canton (today’s Guangzhou). Within that port they were confined to a small physical compound on the riverbank, the “Thirteen Factories.” They were forbidden from learning Chinese, from traveling inland, from staying in the country during the off-season, and from doing business with any Chinese merchant who was not a member of a small state-authorized cartel called the Cohong. The Cohong set the prices. The Cohong arbitrated the disputes. The Cohong reported, when asked, to the imperial bureaucracy. The structural parallel to today’s foreign-investment regime — the negative list, the SAFE controls, the exit bans, the requirement to do business through politically vetted intermediaries — should be obvious to anyone willing to look. The People’s Republic is not inventing anything new. It is running a playbook that is roughly two and a half centuries old, with better software.

The Parsi merchants of nineteenth-century Bombay — the Wadias, the Sassoons, the Jejeebhoys — traded with China extensively, opium for tea, cotton for porcelain, silver for silk. Sir Jamsetjee Jejeebhoy went to China five times. He made one of the largest private fortunes in pre-modern India. He was knighted for it. And he came home with the money. Please note: he came home with the money. He did not buy a building in Canton. He did not set up a permanent Jejeebhoy Office in Shanghai with a five-year lease and a politically connected local partner who would, when the lease expired, point at a building. He went, he traded, he left. Every generation of Parsi merchants for the next century repeated this lesson. The Sassoons did the same. The Wadias did the same. There is a reason these families’ fortunes still exist in Bombay today and not in Guangzhou.

It is also worth pausing on what those fortunes funded. The Bombay Stock Exchange was founded in 1875, which makes it the oldest stock exchange in Asia. It predates the Tokyo Stock Exchange by three years. It predates the Shanghai Stock Exchange by one hundred and fifteen years — Shanghai’s modern exchange opened in 1990, when the People’s Republic of China decided, after forty years of revolutionary anti-market posturing, that perhaps capital markets were not entirely a bourgeois invention. The Shenzhen Stock Exchange also opened in 1990. China’s national capital-markets infrastructure is, in calendar terms, younger than my own children. The BSE is older than my great-grandfather.

And the 1875 founding date understates the case considerably. The BSE was the formal institutional crystallization of merchant-banking and credit arrangements that had been running, in continuous operation, on the Indian subcontinent for centuries before that. The hundi system — the indigenous bill-of-exchange network operated by Marwari, Gujarati, Multani, Bohra, and Chettiar bankers from Kabul to Rangoon — was a fully developed transnational credit instrument by the Mughal era and traces, in its earliest forms, all the way back to the Mauryan and Gupta periods. Which is to say: Indians were running written bills of exchange before England existed as a country. Surat was a recognized banking center in the 1600s, when London was still figuring out joint-stock companies and Amsterdam had only just invented the modern stock exchange. The Jagat Seths of Bengal financed armies and emperors in the eighteenth century; the East India Company itself was, for substantial periods, dependent on Indian banking houses to clear its own transactions. India did not learn capital markets from the British. The British learned a great deal of practical credit management from doing business inside India’s existing one.

Ricardo did not invent comparative advantage. Ricardo described what the Indian merchant class had been operationalizing for two millennia: the principle that everyone gets richer when each region produces what it produces best and trades for the rest. By the early eighteenth century, this had made India approximately twenty-five percent of world GDP — alternating in pole position with China across the imperial centuries, and at points the single largest economy on earth. (I have written about that twenty-five-percent figure in earlier posts.) That share was not extracted from anybody. It was the cumulative output of an open trading civilization doing what open trading civilizations do: selling textiles and spices and steel and gemstones and ships to the world, importing what the world had that it did not, and getting richer over the course of fifteen hundred years. The British did not come to India because India was poor and they wished to develop it. The British came to India because India was rich and they wanted some.

Which means: when the Wall Street fund manager of 2007 looked at India and saw “an emerging market” and looked at China and saw “the future,” he was operating under a fairly stunning misunderstanding of which of the two civilizations had the longer continuous tradition of running actual capital markets. The answer is India, by a margin of approximately three centuries and not really close. The Indian merchant class did not need to be taught what a security was. The Indian merchant class was already doing this in turbans, by hundi, in the seventeenth century, while Europeans were still debating whether interest constituted usury. The Indian capital market is not a 1991 invention or a 1991 recovery. It is a thing India has been doing continuously, with brief state-sponsored interruptions, for roughly four hundred years. The 1991 reforms simply removed the regulatory bandage that the Nehru-Indira state had put on top of the existing system, and the existing system — which had never actually died, only gone underground into informal networks of money-changers, hawala operators, and family-based credit lines — promptly resurfaced and went public.

The Chinese state has, by contrast, no equivalent continuous tradition. The Qing dynasty did not have public capital markets in the modern sense. The Republican period (1912-1949) produced a brief and chaotic flowering of one in Shanghai, which Mao closed in 1949 as a matter of explicit ideological commitment. Forty years later, when the People’s Republic decided it needed capital markets again, it had to build them from scratch — with no living memory of how to run one, no continuous merchant-banking tradition to draw on, and no civilizational disposition that regarded foreign profit-taking as anything other than a temporary indulgence. China’s capital market is forty years old. India’s is, depending on how you count, between one hundred and fifty and four hundred. Both countries have stock exchanges now. Only one of them has a civilizational understanding of what they are for.

The Indian merchant class has absorbed this pattern across generations the way Inuit children absorb the names of the kinds of snow. It is in the muscle memory of the civilization. Any Marwari trading family of any standing would have, in living oral tradition, multiple cousins-of-cousins who had tried to do business in China and come back with a building, or come back with nothing, or not come back at all. The thing the smart money discovered in 2023 — that there is a meaningful, structural, civilizationally-rooted difference between “letting foreigners come and trade” and “letting foreigners come and leave with their winnings“ — was known to my grandmother. It was known to her grandmother. It was known to a substantial fraction of the merchant subcastes of pre-colonial South Asia.

I have, since the early 1990s, told anyone who would listen that this was the wrong trade. I was, for most of those years, treated as a man with an ethnic axe to grind. The axe, it turns out, was a useful piece of inherited equipment.

The thing about pattern recognition, which is what civilizations are for, is that it does not scale through books. Stephen Schwarzman cannot fix his thirty-year-old pattern-recognition problem by endowing a college at Tsinghua. Ray Dalio cannot fix it by reading five hundred years of European empire history. Mark Mobius cannot fix it by being good at cocktail-party storytelling about Indonesian copper mines.

The pattern is in the bones. You either grew up in a civilization that has been on the receiving end of this particular operating system for the better part of two thousand years — in which case the move is obvious from across the room — or you did not, in which case you are going to send your money to Shanghai and a man is going to point at a building.

The East India Company is the standard answer to “well, but India did get colonized, didn’t they?” Yes. India did get colonized. By a British trading company that started in 1608 as a small commercial concession and ended, two and a half centuries later, as the de facto government of the subcontinent. India did not see that one coming. India was, that time, the slow learner.

But India did learn one specific thing. The lesson was not “be open to foreigners,” because India was open to foreigners well before the East India Company arrived and remained open to them well after the British left. India had been open to Greeks, Scythians, Huns, Arabs, Mongols, Persians, Portuguese, Jewish refugees, Zoroastrian refugees, Tibetan refugees, and a substantial number of confused British backpackers, for two millennia before 1608, and continued to be open to all of them after 1947. The openness was not a lesson. The openness was, and is, the operating system.

The thing India learned from the East India Company episode was narrower and more specific: do not let a foreign commercial entity capture the state. Take their investment, tax their profits, make them obey your laws, but do not — under any circumstances — allow a private foreign corporation to acquire its own army and start collecting your revenues. The Indian state in 2026 has many features that an outside observer might reasonably find objectionable, but the one feature it does not have is foreign-corporate sovereignty. Apple cannot raise a regiment. Walmart cannot collect the land tax. The mistake from 1757 to 1857 was not openness. The mistake was openness without sovereignty. India fixed the second part. The first part was never broken.

India then proceeded, in its characteristic way, to make other enormous mistakes — the forty-year socialist autarky described above being the most consequential. Through all of that, the civilization was open. The state was, for a while, deranged. The civilization waited the state out. In 1991, the state corrected itself, partially because the foreign exchange reserves had run down to two weeks of imports and there was no further choice. The civilization always was, and is, open. The state’s forty-year closure was a self-inflicted exception, now corrected.

China’s trajectory has no equivalent of this pattern. China did not open in 1608, get colonized, close down in 1949, briefly re-open in 1979, and remain genuinely open thereafter. China was a closed civilization before the Opium Wars. China was forcibly pried open by Western military violence in the nineteenth century, which it never accepted as legitimate. China resealed itself under Mao. China then announced a “reform and opening” in 1979 that was always — always — designed to be reversible, controlled, sectorally bounded, and revocable at the discretion of the state. The negative list is not new. The capital controls are not new. The exit bans are not new. The hostility to foreign profit-taking is not new. They are continuous with five centuries of Chinese statecraft, briefly interrupted by the period in which the West was strong enough to force the door open and is now strong enough no longer.

China was not open and is not open. China was open in the way a department store is open: you may come in during business hours, browse, purchase under the supervision of staff, and leave through the marked exit. You may not move in. You may not take inventory home. You may not stay past closing. The store reserves the right to refuse service and to keep your coat.

India was open and is open in the way a port city is open: people arrive, people leave, some stay, some get rich, some get robbed, the harbor accepts all comers and the city absorbs whatever the harbor delivers. The British arrived and stayed too long and India had to evict them. That eviction was a correction, not a closing. The door was open before they arrived and the door was open after they left.

One civilization is, civilizationally, a port city. The other civilization is, civilizationally, a department store. Both have been what they are for centuries. The state’s behavior in each case is downstream of what the civilization is.

To put it without the metaphor: the difference is not that one society likes money and the other does not. Everyone likes money. China likes money ferociously. The difference is whether the foreigner is understood as a guest who may leave with his winnings, or as a resource to be managed until the state decides the game is over. India, for all its bureaucratic cruelty, has consistently treated the foreign trader as the first thing. China, for all its reform-era hospitality, has consistently treated him as the second.

The point of this entire post is that the consequences of those two civilizational dispositions are completely predictable, that they have been predictable for centuries, and that a generation of fund managers paid millions of dollars a year to predict things spent thirty years not predicting this one. They were not making a hard call wrong. They were making an easy call wrong. The signal had been transmitted, continuously, for half a millennium. They were not listening for it.

The smart money was not the smart money. It was the inexperienced money, with a Bloomberg terminal.

VIII. The Fifty-Year Bet

Here is what I actually think.

In fifty years, India will be a richer and more prosperous country than China. Not slightly richer. Meaningfully richer. Not in the conventional emerging-markets-catch-up way, in which a low-base country runs faster than a higher-base country for a few decades and then converges. In a structural, civilizational, this-is-how-the-two-countries-are way. I will not be alive in fifty years to be proved right or wrong about this. I am, nevertheless, willing to be on the record now, in 2026, because I have been on the record about everything else in this post since the early 1990s and the only thing that has changed is that the rest of the world is, slowly, catching up.

The inversion has already happened, mechanically. The 2023 numbers tell you the truth in the antiseptic language of the Bureau of Economic Analysis: new US flows to India (6.0billion)exceedednewflowstoChina(5.1 billion) for the first time in the data series. On China’s balance-of-payments measure, inward direct investment turned negative in the third quarter of 2023 and the full-year figure collapsed from its 2021 peak to a fraction of it — the steepest sustained decline in the history of that series. The American Chamber of Commerce in Shanghai’s 2025 survey reported that twelve percent of US firms now rank China as their headquarters’ top investment destination, the lowest figure in the survey’s history. The AmCham China business climate survey for 2025 found only forty-nine percent of US companies expected to be profitable in China that year. Blackstone announced in March 2025 that it would double its India exposure to $100 billion. Even Jim Rogers, in April 2024, finally turned bullish on India.

When Jim Rogers has turned bullish on you, you can be reasonably confident that the trade is no longer contrarian. But that is not the trade I am describing.

The trade I am describing is louder and longer and considerably more lucrative for whoever has the nerve to take it seriously. India will, by 2076, be a richer country than China. Let me be precise about how bold that is. As I write, China’s GDP per capita is roughly five times India’s. China is, today, far ahead — richer, better-built, with newer airports, faster trains, and a manufacturing base India cannot presently approach. Anyone betting on India over a fifty-year horizon is betting against an enormous current lead. I am making that bet anyway, on the record, in 2026. India’s economy will, by the middle of this century, almost certainly be the third largest in the world by nominal GDP, and possibly the second. India’s per-capita wealth will, by 2076, exceed China’s. The reasons are exactly the reasons this entire series has been laying out for twenty installments: a young population, a working democracy, a functional (if maddening) court system, an English-speaking professional class that has placed Indians at the head of a remarkable number of America’s largest companies, an open civilizational disposition that absorbs and metabolizes foreign capital and talent rather than caging it, and a state which — for all its absurdities — does not as a matter of policy disappear foreign executives who write the wrong email. China’s current lead is real, and it is vast. My wager is that it is also, on a fifty-year clock, perishable.

China has, by contrast, an inverted population pyramid that is now in irreversible structural decline, a one-party state under Xi that has spent five years systematically destroying its own most productive sectors, a real estate bubble whose final accounting has not yet been fully done, a youth unemployment rate that the state has, at various points, simply stopped publishing, and a capital regime that has, as this post has documented at length, made it clear to the entire planet that money sent into China is no longer money that may, with full assurance, leave China.

The “smart” money is, in 2026, beginning to act on all of this. Quietly. The Apple manufacturing build-out in Tamil Nadu. The Foxconn factories. The Blackstone India fund. The Walmart-Flipkart hold. The Google Digitization Fund. The Microsoft Azure expansion. The Amazon billions. Every one of these companies is, right now, this quarter, voting with very real money for the thesis that India is the next quarter-century’s growth story. Almost none of them are saying so on television.

This is the actual smart bet. And it is being placed, in size, by the people whose money it is — even when the people whose mouths it is do not yet say so. The question I find myself wondering about, watching this from a desk in Connecticut, is not whether the bet is being placed. The bet is being placed. The question is: how long is it going to take before the smart money gets loud about it?

Because the day the smart money gets loud about India is the day the trade is over for whoever waited for the loudness. The trade is happening now, while Ray Dalio is still writing essays titled “To Answer the Question of Why I Invest in China.” The trade is happening now, while Schwarzman College is still graduating cohorts of Westerners credentialed in the China century. The trade is happening now, in 2026, while the cover stories of the major business magazines are still about Xi Jinping. The capital that gets there before the noise is the capital that captures the run. The capital that arrives after the cover stories arrive late.

I have, since 1991, been on the record. Quietly, in dinner conversations. Loudly, in this Substack, for the past two years. The smart money is, in some sense, finally catching up — which is to say, finally acting. The remaining gap is between what the smart money is doing and what the smart money is saying. I am writing this post, in part, to try to close that gap by a few weeks. The act and the word should move together. The act has moved. The word is dragging.

I will not be alive in 2076 to see India become a richer country than China. I would like, very much, before then, to be alive to see the people who run the world’s largest hedge funds say out loud the thing their own internal investment committees are already, this quarter, voting for. I would like that to happen on a stage. With cameras. I would like it to be the moment Ray Dalio is asked, on a podcast, what his favorite Indian dynasty is, and is not able to come up with a single one, because he hasn’t done the homework yet, again.

We will probably get there. I just hope we get there fast enough that some of the people who have been right about this for thirty years are still around to enjoy it.

Not all of us will be.

IX. The Building Floor, Revisited

My partner, as I mentioned at the beginning of this post, is no longer with us. He died knowing he had been cheated. He died knowing the Chinese court had agreed he had been cheated. He died knowing that none of that was ever going to be made right. Somewhere in some Chinese city, there is a floor of a building that was, in some technical and entirely useless sense, his. He never saw it. He never wanted to see it. He flew home empty-handed once and he never went back. The capital he had wired into the country stayed in the country. The principle of the thing stayed with him until the end. That is a long time to carry a bitter pill, and it is the kind of pill that does not stop being bitter just because the person carrying it has stopped being alive to taste it.

Compare him to Cairn Energy. Cairn lost $1.2 billion to the Indian retrospective tax. Cairn sued in international arbitration. Cairn won. Cairn began seizing French government property held by the Indian state. India, having been thoroughly embarrassed, repealed the law and wrote a check for approximately a billion dollars within a year. Nobody at Cairn died waiting.

This is the choice the smart money spent thirty years getting wrong.

One civilization will offer you a floor in a building, and then it will outlive you, and the floor will still belong to the man who took your money.

The other civilization will, eventually, after enough screaming, write you a check while you are still alive to cash it.

If you want to know which country is going to be rich in fifty years, do not look at where the smart money is currently parking. Look at where the smart money eventually escapes back to with whatever is left of its principal. The smart money, in retrospect, has not been very smart. But the dumb money — the bureaucratic, exasperating, infuriating, court-clogged, audit-happy Indian capital market — has, quietly, been giving people their money back at the end of the dispute. Sometimes after nine years. Sometimes after a dozen. But back, while the people are still here to receive it.

That is what a civilization that wants foreigners to make money looks like, even when it is simultaneously doing everything in its power to make them sweat for it. The sweat is real. The exit is also real. The check, eventually, clears.

For thirty years, I have told anyone who would listen: invest anywhere you want, but not in China. I was a crank. I am, in 2026, slightly less of a crank. The Mark Mobiuses of the world have, belatedly, joined the chair-shortage in the room where the cranks meet. The room is more crowded than it used to be.

There is one chair, in that room, that will always be empty. It belongs to a partner of mine, who did not get to be in the room when the rest of the world figured out what he had figured out the hard way, with his own money, in his own lifetime, in a Chinese courtroom. He is, in some final sense, the reason this post exists. The capital he lost was, in the grand scheme of global FDI flows, not very much. The principle of the thing was, and is, a great deal.

We have a few extra chairs. Henry Kissinger is no longer with us. Mark Mobius, sadly, joined him last month — he died in Singapore, bullish on India to the end, which is the way one would want to go out. We cannot save him a seat. But Kissinger’s blurb-recipients are increasingly welcome. Larry Summers may show up any time. Ray Dalio, if he is reading this — and one assumes that a man who has written six books about his own Principles has a Google Alert for his own name — Ray, the door is open. We have a chair for you too.

Just leave the book on the way in. We have read it.

And on the way in, perhaps, walk past the empty chair. Spend a moment with it. Think about the man who should have been sitting in it. Think about the building in the city he didn’t live in. Think about what it means that the brightest financial minds of our generation sent enormous sums of other people’s money into a system that does this to people, and that some of those people died waiting for the system to be fair to them, and that the people who sent that money are still on television.

Then sit down. We have a lot to talk about.

If you found this essay worth your time, you may enjoy my book The Science of Free Will, which asks an equally uncomfortable question about an equally cherished story.

New to The India Paradox? Start with The Paradox of India, the first essay — or browse the whole series.

Related country-specific work: Albion — Britain’s institutional decline, by someone who first saw the place in 1979.

Wonderful post! Samir is a treat to read. However, plenty of people named Varma have invested in China over the last 35 years & earned about 4 times what they would have in India. But that wasn’t portfolio investment. It was ‘make in China’ & facilitate ‘capital flight’ from China for the sake of ‘guanxi’. In the old days, worthless poets like me were enlisted to get the kids of Chinese bureaucrats into posh British schools & Colleges. Then, greedy Old Etonians & Oxbridge Professors disintermediated lowly darkies like me.

BTW it was McNamara, at the World Bank, & Edwin Lim who gave China this model whereby the Party maximises ‘long term residuary control rights’ (& thus Georgian rents) while minimising constraints on ‘decision rights’ (Hayekian). Initially this was to get the Chinese to adopt best practice Japanese tie-ups for infrastructure. But IP theft was always built in as was no fucking Georgian rents for foreigners. Get rich now. Do Guanxi (i.e facilitate financial and other crime by the nomenklatura) by all means. The benefits stay in the Party.

India is a decent country with a decent but, at times a bit dysfunctional, judiciary. Under Modi, you have Gujarati commercial ethics rather than faith (bhakti) in some idealistic, pro-poor, ideology. I come from Tamil Nadu- where ‘bhakti was born. Gujaratt is where it ‘dies’’ This is nonsense. TN has done well because women’s participation has risen. Mums don’t need no stinkin’ ideology or instructions in ‘Faith’.

I am aware that Samir’s post could be contradicted line line line. Would some minion of Soros or Singham bother to do so? No.

Why? They can’t write as well as Samir.

Modi should find some way to entice the fellow back to India. Alternatively, leave him in place as a more mathsy Sanjeev Sanyal.

Amid a slowing and uncertain global economy,

there are still important signs of resilience.

India continues to stand out as one of the fastest-growing major economies in the world.

The International Monetary Fund has recently raised India’s growth forecast to around 6.5%–6.6%,

reflecting strong confidence in its economic momentum.

This performance is being driven by:

Resilient domestic demand

Expanding exports

And a growing, dynamic market

Excellencies,

At a time when many economies are slowing,

India’s growth highlights an important lesson:

Strong fundamentals and internal demand can provide stability even in global uncertainty.

However, this success also brings responsibility.

Sustaining high growth will require:

Continued investment in infrastructure and industry

Job creation that matches the scale of the workforce

And resilience against external shocks

Because rapid growth is not just about speed

it must also be inclusive, stable, and sustainable.

India’s trajectory offers both opportunity and insight

for the global economy.

In a time of uncertainty,

it reminds us that growth is still possible

with the right balance of policy, investment, and vision.