Disincentivize!

On the most boring, responsible thing ninety-six million Indians are quietly doing — and the strange national reflex that mistakes it for a problem.

Part of The India Paradox. On the most boring, responsible thing ninety-six million Indians are quietly doing — and the strange national reflex that mistakes it for a problem.

Somewhere in India right now, a schoolteacher is putting two thousand rupees into an index fund.

She did not agonize over it. She set up an auto-debit from her salary account three years ago and has thought about it roughly as often as she thinks about her electricity meter. On the fifth of every month the money leaves, buys units, and disappears into the great anonymous machinery of the Nifty. It is the single most boring financial act a human being can perform — the personal-finance equivalent of flossing. No drama, no genius, no timing. Just a small, dull, disciplined transfer, repeated until it compounds into something that might one day be a house, or a daughter’s college, or simply the difference between a frightened old age and a calm one.

And a financial columnist has identified her as a threat to the national currency.

He does not put it that way, of course. He is far too careful and far too intelligent to put it that way, which is precisely what makes the argument worth taking apart. The crude version — the proles are gambling and it’s hurting the rupee— would be easy to dismiss and not worth a thousand words. The version he actually wrote is subtler, partly correct, internally sophisticated, and arrives, with the quiet inevitability of a man reversing confidently into a lake, at a conclusion that would have made Indira Gandhi proud.

His conclusion is that India should disincentivize its citizens from investing in stocks.

This is a real argument, made in good faith, by someone who has himself been a disciplined equity investor for twenty years and who signs off by bracing for abuse. I am not going to abuse him. I am going to do something he will find considerably more irritating, which is agree with him three times before I’m done.

What he gets right (and we must say so)

The series has a rule about this: you do not get to knock down a strawman and call it a victory. So let us build the man’s argument at full strength, because most of it stands.

He is right that foreign money leaving India demands dollars. When a foreign fund sells its Indian shares, it is paid in rupees, and those rupees must be converted into dollars to go home. Multiply that by enough funds over enough years and you get genuine, measurable pressure on the rupee. This is not a theory. The Reserve Bank’s own data on the repatriation of foreign direct investment shows the number climbing steadily, and he reproduces the chart. Concede it cleanly: the dollars are leaving, and it matters.

He is right that a great deal of that repatriation has been venture capitalists and private-equity firms cashing out of loss-making startups at the precise moment those startups listed on the exchange at valuations untethered from anything so vulgar as earnings. This, too, is real. We have all watched a company that has never made a rupee of profit price its IPO as though it were minting them, while the early investors quietly walk through the exit they’d been waiting eight years for.

And he is right — most damning of all, because it’s the part everyone gets wrong — that there is no selling without buying. He says so explicitly. He does not make the lazy error. When a foreign institution dumps a billion dollars of Indian stock, someone has to be standing on the other side of that trade with a billion dollars to catch it. Increasingly, the someone catching it is our schoolteacher and ninety-six million of her countrymen, arriving on the fifth of every month with their two thousand rupees. He has correctly identified that domestic retail money is the counterparty to the foreign exit.

So far, so good. Three concessions, all earned. He understands the plumbing. He is not an idiot, whatever his relatives may say at weddings.

Here is where he reverses into the lake.

The man had the right tool in his hand

Read the column carefully and you find that he has already diagnosed the actual problem and already proposed the correct fix — and then, two paragraphs later, abandons both for something else entirely. This is the part that should make you sit up, because it is the whole tragedy in miniature.

The actual problem, by his own account, is overpriced IPOs. The mechanism is specific and correct: existing regulations let a company list by floating only a small sliver of its equity. When demand for stocks is feverish, that small float lets investment bankers price the whole thing at insane multiples, which lets insiders cash out at valuations that “would have been difficult to justify under normal market conditions.” The disease is not that Indians are buying stocks. The disease is that a structural quirk in listing rules — small mandatory float plus euphoric demand — manufactures inflated exits for a few dozen well-connected sellers.

And he names the cure himself. Raise the minimum public float. Make companies sell a bigger slice when they list, so the price has to reflect something closer to reality and can’t be juiced by artificial scarcity. He even points the finger at the right address: the Securities and Exchange Board of India, which writes those rules and could change them on a Tuesday.

This is a scalpel. It is aimed at the actual tumor. It touches the schoolteacher not at all.

So what does he do with his scalpel? He sets it down on the tray, walks across the room, and picks up a sledgehammer.

Because the recommendation he actually lands on — the one in bold, the one he braces for abuse over — is not “fix the float.” It is: tax all investment income at the same rate. Capital gains on equity should be taxed identically to interest on fixed deposits, gains on gold, gains on real estate. A “level playing field across asset classes,” so that tax considerations no longer “disproportionately influence investment choices.”

He had a tool that hit the investment banker. He swapped it for one that hits the schoolteacher. And the swap was not an accident. It is the most revealing thing in the column, because it is the oldest reflex in the entire Indian policy cabinet, and he reached for it without seeming to notice he’d done it.

The gold trap, and why inert metal is the tell

The bridge he uses to get from the IPO problem to the universal tax is gold — and it’s worth dismantling the bridge, because it’s load-bearing and it doesn’t hold.

His logic runs: India imports nearly all its gold, paying in precious dollars (seventy-two billion of them in 2025-26, more than double three years prior). This is a real drain. Gold-buying has therefore been gently discouraged — higher duties, official tut-tutting, mutual funds restricting gold-fund inflows. So, he reasons, if we discourage gold to protect the rupee, why not discourage excessive stock-buying along the same lines?

Notice what he’s done. He has taken the logic that applies to gold and walked it across to equity. And here he trips over a distinction he himself raises and then waves away. He concedes — in writing — that “gold is largely a useless asset and equity isn’t.” Then he says the distinction “weakens significantly” because so much stock-buying is just funding overpriced insider exits.

But the distinction doesn’t weaken. It is the entire point, and it survives his objection completely intact.

Gold sitting in a locker is inert. It does nothing. It produces no goods, employs no one, builds no factory, funds no payroll. A bar of gold in 2026 will be exactly a bar of gold in 2046, having contributed precisely nothing to the productive capacity of the nation in between. Discouraging it is, at worst, neutral. The gold just sits there being sat upon.

Equity is the opposite of inert. A rupee of equity is a rupee of risk capital locked into a productive enterprise — a company that hires, builds, exports, innovates, and pays corporate tax on its profits before the shareholder is taxed again on his gains. The schoolteacher’s two thousand rupees does not sit in a locker. It becomes working capital. It is the single most useful thing a household can do with its savings from the point of view of the very country he claims to be protecting.

The “overpriced IPO” objection doesn’t change this, because it confuses the price of some equity at the moment of listing with the nature of equity as an asset. Yes, some IPOs are overpriced, and yes, that funds some bad exits. But the cure for an overpriced subset is to fix the pricing mechanism — which, again, he already proposed — not to tax the entire asset class as though it were metal in a vault. You do not discourage everyone from eating because some restaurants overcharge for the bread.

The gold parallel is the tell. The moment you find yourself reasoning “we discouraged the inert thing, so let’s discourage the productive thing by the same logic,” you have stopped thinking about economics and started obeying a reflex. And we know this reflex. We have its photograph.

The experiment already ran. We have the photographs.

Here is the part the column never reckons with, and it is not a matter of theory. It is a matter of what happened three months before he sat down to write.

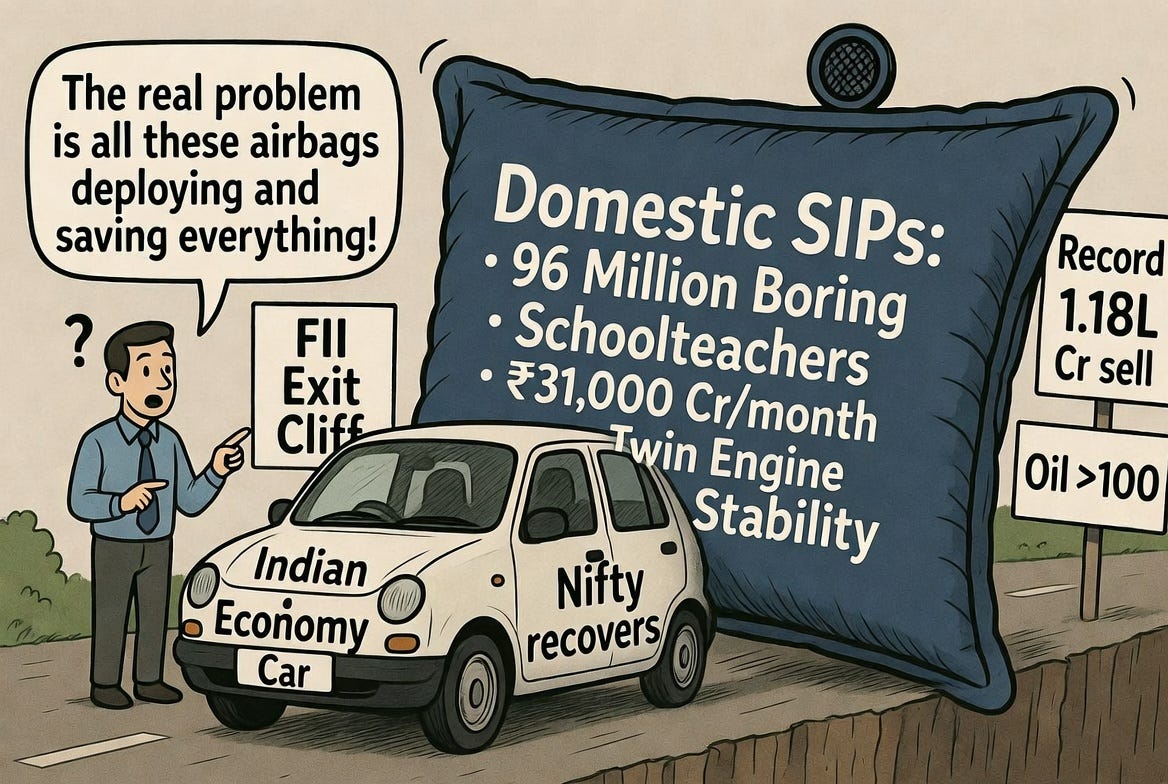

In March 2026, foreign institutional investors sold a record 1.18 lakh crore rupees of Indian equity in a single month — the largest monthly foreign exit on record, larger than the entire foreign inflow of the boom year 2013. The rupee was scraping ninety-four to the dollar. Oil was over a hundred. By every page of the historical playbook, this is the setup for a rout: foreign money stampedes for the door, the market collapses, the currency follows, and India spends the next eighteen months in a defensive crouch composing wounded op-eds.

It didn’t happen.

Domestic institutions — overwhelmingly the mutual funds fed by those boring monthly SIPs — bought 1.16 lakh crore rupees of equity in the same month. They absorbed almost the entire foreign exit, rupee for rupee. The Nifty fell about eleven percent and then steadied. There was no systemic panic. Analysts reached for a new phrase: India had become a twin-engine market, no longer dependent on a single foreign engine that could cut out whenever a fund manager in London got nervous about the Strait of Hormuz.

Sit with that, because it is the exact inversion of his thesis. The SIP money he wants to disincentivize is the precise mechanism that absorbed the foreign exit he is worried about. He has looked at the airbag that just deployed and saved the car, and concluded that the real problem is all these airbags.

And then there is 1991, which this series has told at length and will not retell here, except for one image. In 1991 India had no domestic buffer at all — no twin engine, no schoolteachers, no SIPs. When the dollars ran out, the country airlifted forty-seven tonnes of gold to the Bank of England and another twenty to Switzerland to raise six hundred million dollars and avoid defaulting on its debts. That is what it looks like when a nation has no domestic capital base to lean on: you fly your jewellery to London in the dead of night. We have spent thirty-five years building exactly such a base, household by household, two thousand rupees at a time. It now arrives at the rate of roughly thirty-one thousand crore a month. The proposal on the table is to discourage it, for the rupee’s sake.

He also diagnosed the wrong disease

There’s a second, quieter problem, which is that the thing actually pressuring the rupee in 2026 has very little to do with SIP investors or startup repatriation, and the column would have known this had it looked sideways instead of down.

The dominant driver of the 2026 foreign exit was a global rotation out of Indian equities and into the artificial-intelligence trade. The chips money — the allocation that used to flow to Indian IT — went to Korea and Taiwan instead. That’s structural, and it has nothing to do with our schoolteacher. The second driver was valuation: Indian stocks trading at a forward price-to-earnings ratio around twenty-two while the broad emerging-market index sat near thirteen. A growth premium India has always enjoyed; a gap that size is harder to defend. The rest — rupee at ninety-five, oil over a hundred, the US ten-year yield testing four and a half percent — is cyclical macro weather that will turn when the geopolitics turn.

And the detail that detonates the framing entirely: through all of this, foreign investors were net buyers of the Indian capital-goods and capex story in every single month of 2026. They were not fleeing productive investment. They were trimming overpriced financials and buying the factories. The picture the column paints — foreigners cashing out of loss-making startups as the defining dynamic — was a 2021 story being narrated over a 2026 market that had long since changed the channel. He prescribed poison, and he prescribed it for the one organ that was perfectly healthy.

Now, the economics — and the part where he’s not even in the room

Set aside the plumbing and the photographs for a moment and ask the cleaner question: what does the actual discipline of economics say about taxing capital?

It says, roughly, as little as possible, and the experts can’t agree on how little.

The famous result belongs to Christophe Chamley and Kenneth Judd, who in the mid-1980s, working independently, reached the same startling conclusion within standard growth models: the optimal long-run tax on capital income is zero. The result was so counterintuitive that economists have spent forty years arguing about what it even means — and, this is true and I treasure it, they describe their own models as behaving “erratically” and producing results “of limited use for guiding policy,” which is the most honest thing any profession has ever said about its own flagship theorem. In 2020, Straub and Werning reopened the question and showed that under plausible conditions the optimal capital tax is positive after all — though still, in the serious cases, lower than the tax on labour.

So here is the honest state of the field, the version no economist can dock me for: the entire serious literature on optimal capital taxation lives in a band running from a floor of zero up to a ceiling of “positive, but generally below what you’d tax wages.” Reasonable people argue about where in that band to stand. It is a real, live debate.

His proposal is not in the band. Tax equity gains at the same rate as fixed-deposit interest, as gold, as real estate treats the formation of productive risk capital as identical to the interest on a savings account and the appreciation of metal in a vault. That is not a daring position at the high end of the debate. It is a refusal to attend the debate. He is not wrong within the discipline; he is standing in the parking lot, explaining to the valet why the building is on fire.

But here is the thing — and this is where I have to take the column behind the shed — even that band is too kind to him, because it is measuring the wrong thing entirely.

Every paper in that literature is, at bottom, about revenue: given that the state needs money, what is the least-destructive way to extract it. Which quietly smuggles in an assumption nobody examines — that the number worth maximizing is the government’s haul. And for a poor country sprinting to get rich before it gets old, that is the wrong number. The number that matters is growth. And growth, it turns out, rides a completely different curve.

I’ll keep this painless, because I develop the full version elsewhere and you have a life. Picture two curves. One plots government revenue against the tax rate — the famous Laffer curve, the one that bends back on itself because a 0% rate and a 100% rate both raise exactly nothing (at zero there’s no tax; at a hundred, nobody bothers earning anything to be taxed). Fine. But there is a second curve, which almost nobody bothers to draw, plotting economic growth against the tax rate. It too is pinned at two zeros: at 0% tax there is no government, no courts, no contracts, no roads, so growth is roughly nil; at 100% tax nobody gets out of bed, so growth is also nil. Which means it, too, has a peak — a growth-maximizing rate, sitting somewhere in the middle.

Here is the entire game in one sentence: there is no earthly reason the peak of the revenue curve sits at the same tax rate as the peak of the growth curve. They are two different functions. Expecting them to share an optimum is like assuming the fastest route to the airport must also be the most scenic. Occasionally, by dumb luck. Mostly, no.

And then the detail that turns a debating point into a sledgehammer: growth compounds. A revenue shortfall is a one-time number. A growth shortfall is a rate, and rates, left alone with time, do unspeakable things. Half a percentage point of extra growth, compounded across our schoolteacher’s working life, does not merely trim the alternative — it laps it, then laps it again, then wanders off to see if there’s anything else worth lapping. So once you take compounding seriously, the contest between the two curves stops being a contest. The rate that maximizes revenue in the long runsimply is the growth-maximizing rate, because the largest tax base any government will ever lay its hands on is the one bolted to the economy that grew the fastest.†

Which means the literature’s ceiling — “positive, but below labour” — was a revenue ceiling all along. For a capital-starved economy whose entire purpose in this decade is to accumulate the capital it does not yet have, the right rate sits lower still, shoved back toward the floor by the one force the revenue models forgot to invite to the meeting: compounding.

So our columnist is not merely standing above the band. The band was the wrong band. He has aimed a tax squarely at the single input — capital — whose accumulation is the growth he needs, in the single country that can least afford to discourage it, having reasoned his way there with great care along a curve he did not realize was the wrong curve. It is, in its way, an extraordinary feat of marksmanship. He has shot the one organ keeping the patient alive — from the parking lot, while telling the valet about the fire.

The conclusion he says he isn’t making

He will object, and loudly, that he proposed nothing so dramatic. A modest equalization of rates, he’ll say. A nudge. Hardly Indira Gandhi. I said no such thing.

He’s right. He didn’t. But he doesn’t get to keep the principle and disown its destination.

Because the principle he is actually endorsing is this: when citizens do something productive at a scale that creates demand for dollars, the state should tax it to discourage them. And once that is the principle, the only question left is the dosage — and there is no number printed on the bottle. If a mild tax is good because it gently discourages the rupee-draining behaviour, then a stiffer tax is better, because it discourages more of it. And a punitive tax is better still. Follow the logic where it actually goes and you do not stop at “the same rate as fixed deposits.” You keep climbing, all the way up, until you arrive — breathless, triumphant, brandishing a chart of FDI repatriation — at a 97.75% marginal rate.

We have been to that summit. India planted a flag there in 1973-74, when the top rate hit 97.75% and a citizen who earned a hundred rupees over the threshold was graciously permitted to keep two and a quarter. It was done for reasons that sounded, at the time, every bit as sober and public-spirited as this column: the prosperous must shoulder the burden, private excess must be curbed, the national interest demands restraint. The result was not restraint. The result was that tax evasion became the national pastime, revenue collapsed, and the policy was quietly strangled within a few years, because it turns out that when you tax something at 97.75% people do not line up to pay — they line up to hide.

The columnist is not Indira Gandhi. He is something this series finds far more interesting: a thoughtful, numerate, twenty-year equity investor who has, without quite noticing, picked up the exact instrument she used and is proposing to apply a gentler dose of it. But it is the same instrument. The principle that licenses his nudge is the identical principle that licensed her sledgehammer; they differ only in how hard the arm swings. And a principle whose logical culmination is 97.75% does not have a calibration problem. It has a direction problem. It is pointed the wrong way — and worse, it is pointed the wrong way down the single axis, growth compounded over a lifetime, that decides whether the schoolteacher’s grandchildren are middle-class or merely hopeful.

The bug that keeps shipping

He closed by bracing for abuse — “let the abuse begin.” But the abuse was never the danger, and it isn’t coming, at least not from here.

The danger is that he articulated, out loud, in a well-reasoned column, the single most durable bug in India’s operating system: the deep, autonomic conviction that when the citizenry starts doing something productive at scale, the state’s first instinct should be to find the lever that makes them do less of it. Not to fix the specific distortion — he found that fix and set it down on the tray. Not to target the actual bad actor — the investment banker pricing the garbage IPO sails through entirely untouched. But to reach, by reflex, for the instrument that disciplines the broad mass of ordinary people, because suppressing citizen behaviour is wired more deeply into the machine than targeting the culprit ever was.

This is the Licence Raj in a SIP-shaped costume. It is the same reflex that taxed toothpaste as a luxury, that made you wait eight years for a telephone, that threw out IBM and Coca-Cola to teach foreigners a lesson, that retroactively taxed Vodafone — and then, when the courts and the howls of foreign investors forced a humiliating repeal a decade later, learned precisely nothing from the episode — that demonetized 86% of the currency overnight to catch black money it did not catch. Each time, the costume is new and the reasoning sounds responsible. Each time, the instinct underneath is identical: the energy of a hundred million ordinary Indians, doing the dull and disciplined thing, treated as a leak to be plugged rather than as the entire point of the exercise.

He won’t get abuse. He’s too smart, and he’s mostly right about the diagnosis, and being mostly right is exactly how the dangerous ideas get past the bouncer. What he’ll get, if the bug ever ships to production, is a policy paper, and a committee, and possibly an award — and our schoolteacher, on the fifth of some future month, will find that the most boring and responsible thing she could possibly do with her two thousand rupees has been gently, fairly, neutrally made a little less worth doing.

For her sake, and the rupee’s, I hope SEBI just fixes the float.

†A caveat for the one reader already sharpening a reply: this holds cleanly where the tax simply discourages productive activity — which is precisely what is proposed here. If the revenue were spent building roads and schools that themselves raise growth, the very low end of the rate gets muddier. But “disincentivize” is not a plan to fund human capital. It is a plan to do less of the thing. The deadweight case is the one in front of us.

The growth-versus-revenue argument — and the four separate nonlinearities that quietly turn almost every tax debate you will ever hear into a confused argument about the wrong curve — gets a full chapter in The Science of Free Will (US · India · UK). Yes, it is a book about free will that contains a chapter on the Laffer curve. It makes sense in context. Mostly.

Great article! People don’t make this point very often because how much the compounding part gets missed. Another failure to grasp the exponential but Covid proved that happens to the best of us.

Having said that, I feel like an even deeper flaw is tying the state’s or the citizen’s ego to the value of the currency. It should be understood as simply a shock absorber reacting to external stimuli and dispersing knowledge to the internal economic actors to adjust their import/export behavior. Linking a nice article making that point here → https://substack.com/home/post/p-198232271